Kudos to Fundstrat’s ever-bullish Tom Lee, one of many few to accurately predict Wednesday’s dovish flip from the Federal Reserve that has unleashed bond and inventory bulls.

As Lee stated on X: “Powell no longer invoking Volcker— risk-on,” in reference to the ex-Fed chief who fought inflation so laborious he triggered a recession. The memes (this one relayed from Macro Tourist’s Kevin Muir) have it:

Lee, by the way accurately known as the 2023 fairness rally and alongside Oppenheimer, holds essentially the most bullish S&P 500 forecast for 2024 of 5,200.

Onto our name of the day, from Jeff Gundlach, chief funding officer and founding father of DoubleLine Capital, who expects the 10-year Treasury yield

BX:TMUBMUSD10Y

— down an additional 8 foundation factors on Thursday at 3.946% — to hit “the low threes by the end of next year.”

Gundlach made his feedback in a CNBC interview late Wednesday, as he predicted unemployment will shoot up subsequent yr and inflation dip to 2.4% by June, triggering a price lower. “The economy is going to undershoot the downside and that is going to create a response. We will have to have a lot of money printing.”

Incidentally, Bill Gross, the billionaire investor and Pimco co-founder, doesn’t agree with Gundlach, saying in an X remark that 3% Treasury yields are “farcical.” Given a typical time period premium, the Fed chopping charges down to three% would imply the 10-year could be round 4%, Gross stated.

Meanwhile, Gundlach weighed in on the bullish market response within the Fed’s wake. “I just think the everything rally concept is a realization of what’s happened in the past six weeks, and we kind of expected that,” he stated.

While the Fed was “pivotish,” in November, which kicked off the inventory and bond rally, a full pivot has now been made, says Gundlach. And as “we’re getting late in the cycle,” greater credit score sectors — not funding grade — “double B sectors” or junk sector components of the bond market are price a glance.

Gundlach isn’t as optimistic on the inventory market.

Gundlach invoked an outdated market saying. “Stocks need bonds, but bonds don’t need stocks. And right now stocks are needing bonds and they’re getting it. But we’ll get into that phase I think in the second quarter or so next year where bonds don’t need stocks, but stocks won’t be participating the way bonds will. So that’s how I think about the pivot, but I also think it’s going to be a year for of great volatility in 2024,” he stated.

Read: Wall Street has found what’s actually driving U.S. shares greater in 2023. The clarification isn’t so simple as one would possibly anticipate.

And to how a lot the Fed will lower subsequent yr, the talk is thick and heavy, with eyebrows raised as markets are pricing in as much as six cuts.

A Goldman Sachs staff led by Jan Hatzius stated they see “earlier and faster” strikes — three straight 25 foundation factors cuts in March, May and June.

“Financial conditions eased further today, and we are more confident that the large easing since October will prove durable now that the lower inflation path makes substantial rate cuts more likely next year,” stated the Goldman staff.

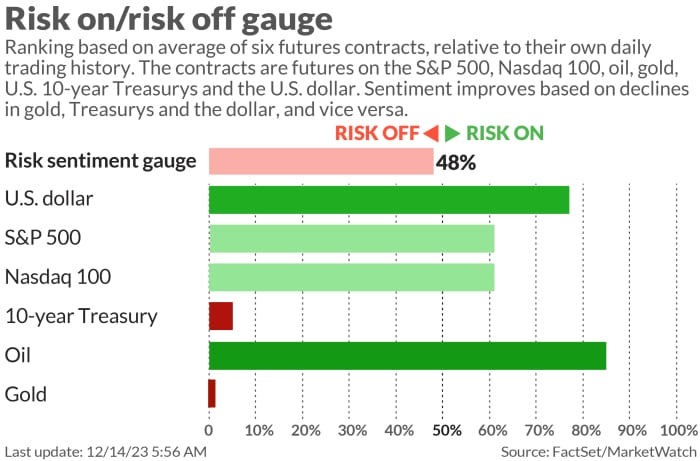

The markets

Stock futures

ES00,

YM00,

NQ00,

are up, with the Dow

DJIA

set for a recent file. Bond yields

BX:TMUBMUSD02Y

BX:TMUBMUSD30Y

are at recent multimonth lows, as gold costs

GC00,

climb over 2% to $2,050 per ounce. The pound

GBPUSD,

shot up after the Bank of England left rates of interest unchanged, however stated they’d want to remain greater for an “extended period.” The European Central Bank additionally held regular.

Follow the motion in MarketWatch’s Live Blog.

Oil costs

CL.1,

BRN00,

are up 2%. The International Energy Agency stated oil demand will weaken subsequent yr.

The buzz

Weekly jobless claims, import costs and retail gross sales are all due at 8:30 a.m., with enterprise inventories at 10 a.m.

Adobe

ADBE,

delivered a disappointing outlook and revealed an Federal Trade Commission probe, with shares down.

Moderna

MRNA,

jumped 7% the biotech and companion Merck

MRK,

introduced constructive information from a mid-stage trial of a mixed therapy for superior melanoma.

Occidental Petroleum

OXY,

is getting a lift from news Berkshire Hathaway

BRK.A,

BRK.B,

purchased the shares on Dec. 11, the identical day the oil producer stated it was shopping for CrownRock. Staying in that sector, BP

BP,

BP,

was lower to underweight from impartial at JPMorgan.

Lennar

LEN,

and Costco

COST,

will report outcomes after the shut.

Russian President Vladimir Putin stated there might be no second name up for reserves and his Ukraine “de-Nazification” objectives stay the identical.

Best of the net

Range Rovers change into thief-magnets, inflicting costs to tumble.

Bill Ackman’s conflict with Harvard reveals messy world of huge donations.

Oprah says the easiest way to drop pounds is ‘everything,’ together with medicine.

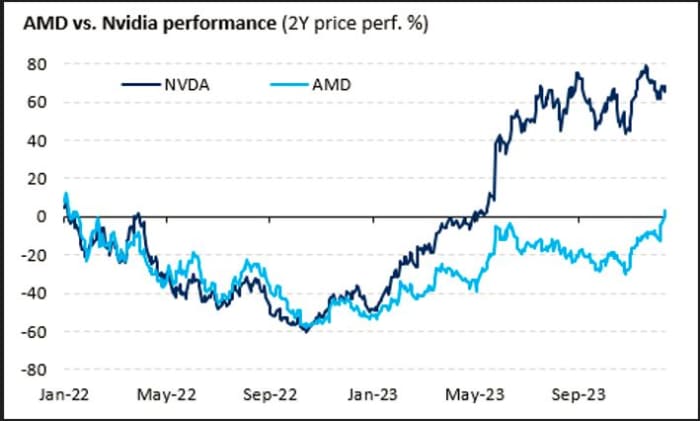

The chart

Move over Nvidia

NVDA,

retail traders are falling in love with different semiconductors, comparable to Advanced Micro Devices

AMD,

says the Vanda Research staff. Here’s their chart:

And if Fed members don’t push again on that dovish Wednesday message, then AMD’s good points could solely develop because it has “significantly lagged” Nvidia’s 2023 climb, says Vanda. And if semi shares momentum “persists, then individual traders could easily make AMD their new #1 pick as they attempt to push the stock to close the gap with its main competitor,” they stated.

Top tickers

These had been the top-searched tickers on MarketWatch as of 6 a.m.:

| Ticker | Security identify |

|

TSLA, |

Tesla |

|

GME, |

GameStop |

|

NVDA, |

Nvidia |

|

AAPL, |

Apple |

|

NIO, |

Nio |

|

AMC, |

AMC Entertainment |

|

AMZN, |

Amazon |

|

MSFT, |

Microsoft |

|

AMD, |

Advanced Micro Devices |

|

PLTR, |

Palantir |

Random reads

This dolphin has thumbs.

Early riser? That’s the Neanderthal in you.

Brenda Lee talks chart-topping at 78

Need to Know begins early and is up to date till the opening bell, however enroll right here to get it delivered as soon as to your e-mail field. The emailed model might be despatched out at about 7:30 a.m. Eastern.

Source web site: www.marketwatch.com