A development in a multifamily and single household residential housing advanced is proven within the Rancho Penasquitos neighborhood, in San Diego, California, September 19, 2023.

Mike Blake | Reuters

In principle, getting inflation nearer to the Federal Reserve’s 2% goal does not sound terribly tough.

The predominant culprits are associated to providers and shelter prices, with lots of the different parts displaying noticeable indicators of easing. So focusing on simply two areas of the financial system does not seem to be a gargantuan process in comparison with, say, the summer season of 2022, when principally all the pieces was going up.

In follow, although, it could possibly be tougher than it seems.

Prices in these two pivotal parts have confirmed to be stickier than another issues like meals and fuel and even used and new automobiles, all of which are typically cyclical as they rise and fall with the ebbs and flows of the broader financial system.

Instead, getting higher management of rents, medical care providers and the like might take … properly, you won’t wish to know.

“You need a recession,” stated Steven Blitz, chief U.S. economist at GlobalData TS Lombard. “You’re not going to magically get down to 2%.”

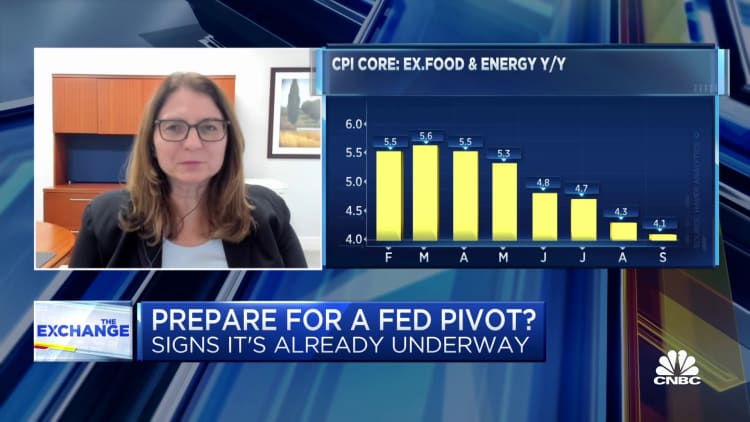

Annual inflation as measured by the buyer worth index fell to three.7% in September, or 4.1% when you kick out unstable meals and power prices, the latter of which has been rising steadily of late. While each numbers are nonetheless properly forward of the Fed’s objective, they characterize progress from the times when headline inflation was operating north of 9%.

The CPI parts, although, instructed of uneven progress, helped alongside by an easing in gadgets reminiscent of used car costs and medical care providers however hampered by sharp will increase in shelter (7.2%) and providers (5.7% excluding power providers).

Drilling down additional, hire of shelter additionally rose 7.2%, hire of major residence was up 7.4%, and homeowners’ equal hire, pivotal figures within the CPI computation that signifies what owners assume they might get for his or her properties on the rental market, elevated 7.1%, together with a 0.6% achieve in September.

Without progress on these fronts, there’s little likelihood of the Fed attaining its objective anytime quickly.

Uncertainty forward

“The forces that are driving the disinflation among the various bits and micro pieces of the index eventually give way to the broader macro force, which is rising, which is above-trend growth and low unemployment,” Blitz stated. “Eventually that will prevail until a recession comes in, and and that’s it, there’s nothing really much more to say than that.”

On the brilliant aspect, Blitz is among the many consensus that sees any recession being pretty shallow and brief. Even extra so, many Wall Street economists, Goldman Sachs amongst them, are coming round to the view that the much-anticipated recession might not even occur.

In the interim, although, is uncertainty.

“Sticky-price” inflation, a measure of issues reminiscent of rents, varied providers and insurance coverage prices, ran at a 5.1% tempo in September, down a full proportion level from May, based on the Cleveland Fed. Flexible CPI, together with meals, power, car prices and attire, ran at only a 1% fee. Both characterize progress, however nonetheless not a objective achieved.

Markets are puzzling over what the Fed’s subsequent step might be: Do policymakers slap on one other fee hike for good measure earlier than the tip of the 12 months, or do they merely keep on with the comparatively new higher-for-longer script as they watch the inflation dynamics unfold?

“Inflation that is stuck at 3.7%, coupled with the strong September employment report, could be enough to prompt the Fed to indeed go for one more rate hike this year,” stated Lisa Sturtevant, chief economist for Bright MLS, a Maryland-based actual property providers agency. “Housing is the key driver of the elevated inflation numbers.”

Higher rates of interest have made their largest affect on the housing market by way of gross sales and financing prices. Yet costs are nonetheless elevated, with concern that the excessive charges will deter development of recent residences and hold provide constrained.

Those elements “will only lead to higher rental prices and worsening affordability conditions in the long run,” wrote Christopher Bruen, senior director of analysis on the National Multifamily Housing Council. “Rising rates threaten the strength of the broader job market and economy, which has not yet fully digested the rate hikes already enacted.”

Longer-run considerations

The notion that fee will increase totaling 5.25 proportion factors have but to wind their means by way of the financial system is one issue that would hold the Fed on maintain.

That, nonetheless, goes again to the concept that the financial system nonetheless wants to chill earlier than the Fed can full the ultimate mile of its race to convey down inflation to focus on.

One constructive within the central financial institution’s favor is that pandemic-related elements largely have washed out of the financial system, however different elements linger.

“Pandemic-era effects have a natural gravitational pull and we’ve seen that take place over the course of the year,” stated Marta Norton, chief funding officer for the Americas at Morningstar Wealth. “However, bringing inflation the remainder of the distance to the 2% target requires economic cooling, no easy feat, given fiscal easing, the strength of the consumer, and the general financial health in the corporate sector.”

Policymakers have been banking on the notion that when current rental leases expire, they are going to be renegotiated at decrease costs, bringing down shelter inflation. However, the rising shelter and homeowners equal hire numbers present that could possibly be an extended log despite the fact that so-called asking hire inflation is easing, stated Stephen Juneau, U.S. economist at Bank of America.

“Therefore, we must wait for more data to see if this is just a blip or if there is something more fundamental driving the increase such as higher rent increases in larger cities offsetting softer increases in smaller cities,” Juneau stated in a word to purchasers Thursday. He added that the CPI report “is a reminder that we do not have good historic examples to lean on” for long-term patterns in hire inflation.

Source web site: www.cnbc.com