The 60/40 stock-bond portfolio, given up for useless in recent times, is outperforming nearly all the subtle endowment portfolios at elite academic establishments.

Read: ‘We’re not in Kansas anymore’: Why the 60/40 portfolio may be useless, and what to do now

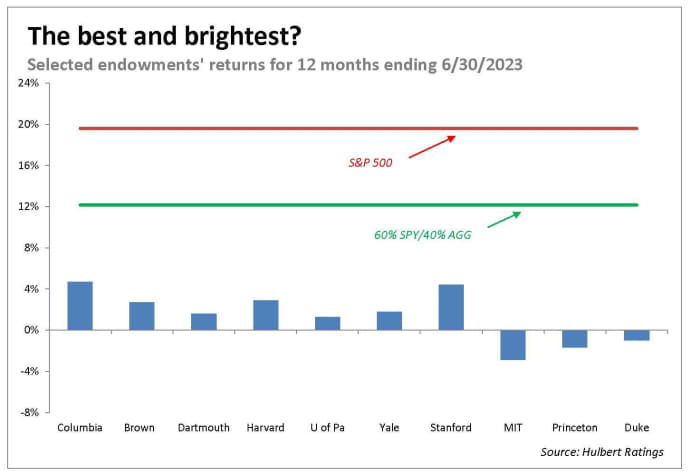

It’s not even shut, in keeping with outcomes launched this week by most faculties and universities for his or her fiscal years ending June 30. In distinction to a 12.2% return for a plain-vanilla 60/40 portfolio, Ivy League college endowments produced returns within the low single digits — in the event that they made any cash in any respect. This is illustrated within the chart beneath.

The longer-term view paints solely a slightly higher image. I calculate that the median faculty and college endowment has lagged behind the 60/40 portfolio during the last 5-, 10- and 15-year durations by margins within the vary of two to 4 annualized proportion factors. The endowment returns are from the National Association of College and University Business Officers.

Opinion: Sell the S&P 500. Buy this as an alternative.

How might these “best and brightest” establishments so considerably lag the general public markets? One of the most important causes nearly actually is that faculty and college endowments have shifted away from the general public inventory and bond markets and invested closely in various investments. They little doubt have been seduced by the massive success of Yale’s endowment within the Eighties and Nineteen Nineties below the well-known path of the late David Swensen.

Harvard’s endowment, for instance, has simply 11% invested in public fairness and 6% in bonds, in keeping with N.P. Narvekar, the CEO of Harvard Management Company, which manages the college’s endowment. Almost all different faculty and college endowments have a equally low allocation to public markets and excessive allocation to various belongings. This is why their newest fiscal-year returns are so intently clustered collectively.

The big inflow of recent cash into various belongings killed the goose that lays the golden egg, in keeping with William Bernstein of EfficientFrontier.com, the writer of the 2010 e book “The Four Pillars of Investing.”

“Swensen got to the alternatives banquet table first and loaded up on lobster tails and prime rib,” Bernstein wrote in an e mail, “and those who followed … got the tuna noodle casserole.”

To illustrate his level, Bernstein asks us to think about that, 25 or so years in the past, roughly $300 billion was invested in hedge funds, and so they collectively went after roughly $30 billion of accessible “alpha.” He says that these numbers, whereas crude estimates, are order-of-magnitude correct.

“That’s 10% of excess return, which covered the 2 and 20,” he mentioned, referring to hedge-fund charges of two% of belongings below administration and 20% of income. “Now there’s $3 trillion chasing the same (or likely less) alpha [and] the excess [alpha] is only 1%.” That isn’t even sufficient to pay the hedge-fund charges, after all.

There’s some solace for the remainder of us in these mediocre or worse endowment returns. We’ve not been lacking out by not being given as a lot entry as massive establishments must hedge funds and private-equity funds. We could even be much better off.

Mark Hulbert is a daily contributor to MarketWatch. His Hulbert Ratings tracks funding newsletters that pay a flat payment to be audited. He may be reached at mark@hulbertratings.com.

Source web site: www.marketwatch.com