Stock buyers have gotten off to a wobbly begin to the brand new 12 months, hobbled by shifting expectations on the timing and extent of Federal Reserve interest-rate cuts in 2024.

All three main U.S. inventory indexes snapped a nine-week successful streak on Friday, after unexpectedly robust December job good points prompted merchants to briefly pull again on the possibilities of a March fee minimize. The S&P 500

SPX

and Nasdaq Composite

COMP

additionally didn’t stage a Santa Claus Rally from the 5 ultimate buying and selling days of 2023 by the primary two periods of 2024, as questions grew in regards to the market’s a number of rate-cuts view.

It all provides as much as a glimpse of what is likely to be in retailer for buyers within the 12 months forward. Already, the so-called “January effect,” or principle that shares are likely to rise by extra now than some other month, could possibly be put to the take a look at by headwinds that embrace stalling progress on inflation. Inflation’s downward pattern in current months had given merchants and buyers hope that as many as six or seven quarter-percentage-point fee cuts from the Federal Reserve could possibly be delivered in 2024, beginning in March.

Over the primary handful of days within the new 12 months, nevertheless, actuality has began to sink in. For one factor, a number of fee cuts are typically extra generally related to recessions and never delicate landings for the economic system.

Moreover, the concept that the Fed might comply with by with as many fee cuts as envisioned by merchants would considerably improve the likelihood that policymakers lose their battle in opposition to inflation, in line with Mike Sanders, head of mounted earnings at Wisconsin-based Madison Investments, which manages $23 billion in belongings. That’s as a result of six or extra fee cuts would loosen monetary situations by an excessive amount of, and enhance the danger of one other bout of inflation that forces officers to hike once more, he stated.

Minutes of the Fed’s Dec. 12-13 assembly present that policymakers had been unsure about their forecasts for fee cuts this 12 months and didn’t rule out the potential for additional fee hikes. Nonetheless, fed funds futures merchants continued to cling to expectations for an enormous decline in borrowing prices, with the best probability now coalescing round 5 – 6 quarter-point fee cuts that whole 125 or 150 foundation factors of easing by year-end. That’s roughly twice as a lot as what policymakers penciled in final month, once they voted to maintain rates of interest at a 22-year excessive of 5.25% to five.5%.

Source: CME FedWatch Tool, as of Jan. 5.

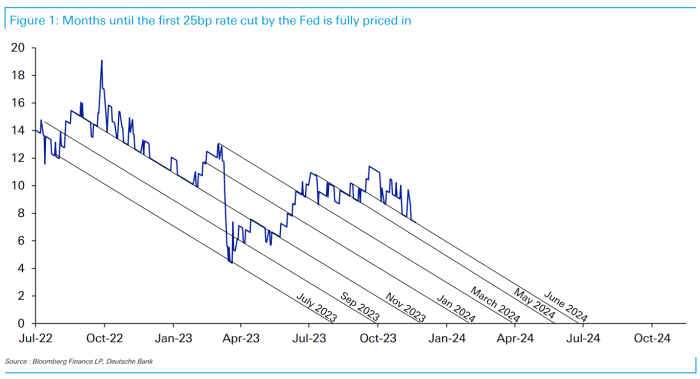

Uncertainty over the trail of U.S. rates of interest might go away buyers flat-footed as soon as once more, and damp the optimism that despatched all three main inventory indexes in 2023 to their greatest annual performances of the prior two to a few years. In November, analysts at Deutsche Bank AG

DB,

counted seven occasions since 2021 through which markets anticipated the Fed to make a dovish pivot, solely to be flawed.

Sources: Bloomberg, Deutsche Bank. Chart is as of Nov. 20, 2023.

Financial markets have been working with “sky-high expectations” for 2024 fee cuts, however the one option to substantiate six cuts this 12 months is with an “abrupt and sharp downturn in the economy,” stated Todd Thompson, managing director and portfolio co-manager at Reams Asset Management in Indianapolis, which oversees $27 billion.

Heading into 2024, euphoria over the prospect of decrease borrowing prices produced what Thompson calls “an alarming, everything rally,” which he says leaves equities and high-yield company debt weak to pullbacks between now and the subsequent six months. Beyond that interval, nevertheless, “the trend is likely to be lower rates as the economy finally succumbs to tightening conditions at the same time inflation continues to recede.”

The coming week brings the subsequent main U.S. inflation replace, with December’s shopper worth index report launched on Thursday. The annual headline fee of inflation from CPI has slowed to three.1% in November from a peak of 9.1% in June 2022. In addition, the core fee from the Fed’s favourite inflation gauge, generally known as the PCE, has eased to 3.2% year-on-year in November from a 4.2% annual fee in July.

The Fed must preserve rates of interest larger due to all of the uncertainty round inflation’s almost certainly path ahead, and the U.S. labor market “won’t degrade fast enough in the first quarter to justify a first rate cut in March,” in line with Sanders of Madison Investments.

Rate-cut expectations are “going to be the issue for 2024, and a lot of it is going to be revolving around inflation getting back to that 2% target,” Sanders stated by way of telephone. “We think somewhere between 75 and 125 basis points of rate cuts make sense, and that the first move is more of a June-type of event. We don’t think it makes sense to have a March rate cut unless the labor market falls off a cliff.”

History exhibits that Treasury yields are likely to fall within the months main as much as the primary fee minimize of a Fed easing cycle. However, that isn’t taking place proper now. Yields on authorities debt have been on an upward pattern for the reason that finish of December, with 2-

BX:TMUBMUSD02Y,

10-

BX:TMUBMUSD10Y,

and 30-year yields

BX:TMUBMUSD30Y

ending Friday at their highest ranges in additional than two to a few weeks.

See additionally: What historical past says about shares and the bond market forward of a primary Fed fee minimize

While monetary markets usually are typically environment friendly processors of data, they “haven’t been very accurate in terms of pricing in rate cuts” this time, stated Lawrence Gillum, the Charlotte, North Carolina-based chief fixed-income strategist for broker-dealer for LPL Financial. He stated the large danger for 2024 is that if monetary situations ease an excessive amount of and the Fed declares victory on inflation too quickly, which might reignite worth pressures in a fashion harking back to the Seventies interval underneath former Fed Chairman Arthur Burns.

“We think rate-cut expectations have gone too far too fast, and that the backup in yields we are seeing right now is the market acknowledging that maybe rate cuts are not going to be as aggressive as what was priced in,” Gillum stated by way of telephone.

December’s CPI report on Thursday is the info spotlight of the week forward.

On Monday, consumer-credit knowledge for November is ready to be launched, adopted the subsequent day by trade-deficit figures for a similar month.

Wednesday brings the wholesale-inventories report for November and remarks by New York Fed President John Williams.

Initial weekly jobless claims are launched on Thursday. On Friday, the producer worth index for December comes out.

Source web site: www.marketwatch.com